4.6 Interest Calculation:

Banks and post offices pay a nominal interest on the balance in SB accounts. The interest % varies from time to time. In the case of Banks it is fixed by Reserve Bank of India and hence it is uniform for all Banks. In the case of Post Office, interest% is fixed by Finance Department of Government of India. It has been 3.5% for many years.

In the case of Banks and also Post Offices, the interest is calculated on the basis of monthly minimum balance maintained between 10th and the last day of each month. But From April 2010, Banks are calculating SB interest on balance held at the end of every day.

4.6.1 Interest on Savings Bank Account in Banks:

In the case of Banks the interest is calculated monthly but credited to the SB account quarterly or half yearly. Method of finding out monthly minimum balance:

Let us assume that an individual has following balances in the month of February of 2004 in his SB account in a Bank

|

Dates |

Account Balance |

No of Days with same balance |

Balance in single day |

|

On 1st,2nd,3rd,4th,5th |

2000 |

5 |

10,000(=2000*5) |

|

On 6th ,7th,8th,9th |

2500 |

4 |

10,000(=2500*4) |

|

On 10th |

2200 |

1 |

2,200(=2200*1) |

|

On 11th to 20th |

3000 |

10 |

30,000(=3000*10) |

|

21st to 25th |

2600 |

5 |

13,000(=2600*5) |

|

26th to 28th |

1400 |

3 |

5,200(=1400*3) |

|

29th |

1300 |

1 |

1,300(=1300*1) |

|

Total |

29 |

71,700 |

|

The lowest daily balance from 10th to last of day of the month (29th) is Rs 1300.

Hence the interest of 3.5% is paid for February month on Rs 1300 for one month (On Rs39,000(=1300*30) for 1 day),though on many days the account had balance more than this amount. Effective from April 2010, in the banks, SB interest @3.5% is paid on Rs 71,700 for one day, as if this amount is in the account for just one day.

4.6.1 Problem 1:

Let the monthly minimum balance for April 2006(Minimum daily balance between 10th and 30th in April) be 2000.

Let the monthly minimum balance for May 2006 (Minimum daily balance between 10th and 31st in May) be 2400.

Let the monthly minimum balance for June 2006 (Minimum daily balance between 10th and 30th in June) be 1600.

Solution :

Since the interest is calculated monthly in every quarter of the year (totally four quarters in a year), the banks use a term called product for easy calculation

‘Product’ is defined as sum of the three monthly minimum balances of three months in a quarter.

In the above Problem

Product = 2000+2400+1600= 6000. Interest at the rate of 3.5% is calculated on this product for one month and the amount is credited to the SB account on 1st month of next quarter (i.e. July)

For interest calculation we use the following formula

Interest = P*(N/12)*(R/100)

Where

P = Principal (Product)

N =Period(one month: 1/12 of year)

R = Rate of Interest

Since rate of SB interest is 3.5%

Interest = P*(N/12)*(R/100) = 6000*(1/12)*(3.5/100)= Rs 17.5

This amount of Rs 17.5 is credited to the SB account on 1st day of the next month (i.e. July 2006)

In banks instead of using formula each time, they use a ready Reckoner (Pre calculated table of interest for different amount and interest rate) similar to the one given below

|

Principal(Rs.) |

Rate@ 3.5% Per Annum |

Rate@ 4% Per Annum |

|

1 |

0.0029 |

0.0033 |

|

2 |

0.0058 |

0.0067 |

|

5,……. |

0.0146 |

0.0167 |

|

……. |

……. |

…… |

|

10 …… |

0.0292 |

0.0333 |

|

……. |

……. |

…… |

|

100 |

0.2917 |

0.3333 |

|

……. |

……. |

…… |

|

1000 |

2.9167 |

3.3333 |

|

2000 |

5.83333 |

6.6667 |

|

3000 |

8.7500 |

10.000 |

|

4000 |

11.667 |

13.333 |

|

5000 |

14.5833 |

16.667 |

|

10000 |

29.1667 |

33.3333 |

|

|

|

|

In the above Problem 6000 can be split as 5000+1000

From the Ready Reckoner for 3.5% we note that interest for one month, for Rs 5000 it is 14.5833 and for Rs 1000 it is 2.9167

![]() Interest for 6000

= Interest for 5000+ Interest for 5000 = 14.5833+2.9167 =17.5.

Interest for 6000

= Interest for 5000+ Interest for 5000 = 14.5833+2.9167 =17.5.

Was not this the result we got using the formula?

Schedule for crediting of SB interest in Banks:

|

Interest for the months of |

Interest credit date |

|

January, February, March |

On April 1st |

|

April, May, June |

On July 1st |

|

July, August, September |

On October 1st |

|

October, November, December |

On January 1st |

4.6.1 Problem 2 : The following are extracts a SB account holder in Karnataka Bank. Check the correctness of SB interest calculated by bank for the quarter (April, May and June 98) if the SB rate of interest is 4%

|

Date |

Particulars |

Debit(-) |

Credit(+) |

Balance |

|

1/4/98 |

Opening |

- |

|

1500.00 |

|

9/4/98 |

To cheque |

300 |

|

1200.00 |

|

10/4/98 |

By Cash |

|

100.00 |

1300.00 |

|

10/4/98 |

To Cheque |

200.00 |

|

1100.00 |

|

1/6/98 |

By cheque |

|

300.00 |

1400.00 |

|

15/6/98 |

By cash |

|

300.00 |

1700.00 |

|

1/7/98 |

By SB interest |

|

12.00 |

1712.00 |

Solution:

Let us find now the Monthly minimum balance for the three months starting from April 98.

|

No. |

Month |

Lowest balance |

Explanation |

|

1 |

April’98 |

1100 |

On April 10th there were two transactions and the lowest of the two balances is 1100 |

|

2 |

May’98 |

1100 |

May did not have any transactions and hence the balance on all days in May was 1100 |

|

3 |

June’98 |

1400 |

Rs 300 was deposited after 10th of June |

|

|

Product |

3600 |

|

It is given that rate of interest is 4%

![]() Interest =

P*(N/12)*(R/100) = 3600*(1/12)*(4/100) = 12

Interest =

P*(N/12)*(R/100) = 3600*(1/12)*(4/100) = 12

This amount of SB interest was correctly credited by the bank to the account on 1st July 98, From July onwards; the SB interest credited to the account is also included for monthly SB interest calculation.

Note :

Interest earned on a deposit of Rs 5000 for 30 days is equal to interest earned on a deposit of 1,50,000(=5000*30) for one day

(![]() 5000*30 days =

150000*1day)

5000*30 days =

150000*1day)

Similarly interest earned on a deposit of Rs5, 000 for 12 months is equal to interest earned on a deposit of Rs.60, 000(=5000*12) for one month.

(![]() 5000*12 months =

60000*1 month)

5000*12 months =

60000*1 month)

4.6.2 Interest on Savings Bank account in Post offices:

In post offices also the method of calculating SB interest is same as in Banks but the interest is credited only once a year on 1st of April. The monthly minimum balance in Post office is called ‘Interest bearing balance’ which is the lowest of daily balances between 10th and the last day of any month.

The SB interest can be calculated using the formula or Ready Reckoner

4.6.2 Problem 1 : Madhuri has a post office SB account. The following are extracts of her pass book. Find out the interest which gets credited to her account on 01/04/2000 if rate of SB interest is 4%.

|

Date |

Debit(-) |

Credit(+) |

Balance |

|

1/4/99 |

- |

20.00 |

20.00 |

|

6/5/99 |

|

275.00 |

295.00 |

|

18/6/99 |

22.00 |

|

273.00 |

|

26/6/99 |

|

108.00 |

381.00 |

|

7/7/99 |

|

113.00 |

494.00 |

|

7/8/99 |

24.00 |

|

470.00 |

|

12/10/99 |

17.00 |

|

453.00 |

|

5/11/99 |

|

130.00 |

583.00 |

|

11/12/99 |

|

105.00 |

688.00 |

|

8/1/2000 |

95.00 |

|

593.00 |

|

22/2/2000 |

210.00 |

|

383.00 |

|

10/3/2000 |

|

38.00 |

421.00 |

Solution:

Let us find now the ‘Interest bearing balance’ (IBB) for all the 12 months starting from April 99 to March 2000

|

No. |

Month |

Lowest balance |

Explanation |

|

April’99 |

20 |

|

|

|

2 |

May’99 |

295 |

|

|

3 |

June’99 |

273 |

Rs 108 was deposited after 10th |

|

4 |

July’99 |

494 |

|

|

5 |

August’99 |

470 |

|

|

6 |

September’99 |

470 |

There was no deposit or withdrawal in September |

|

7 |

October’99 |

453 |

On 10/10 the balance was 470 |

|

8 |

November’99 |

583 |

|

|

9 |

December’99 |

583 |

Rs 105 was deposited after 10/12 |

|

10 |

January’2000 |

593 |

|

|

11 |

February’2000 |

383 |

|

|

12 |

March’2000 |

421 |

|

|

|

Total IBB |

5038 |

|

We have seen that

Interest = P*(N/12)*(R/100) = 5038*(1/12)*(4/100)= Rs 16.79

This amount will be credited by post office on 1/04/2000 to the SB account of Madhuri

Exercise : Verify that you will get same interest if you use Ready Reckoner maintained in post offices for 4% interest (for using ready reckoner,split 5038 as 5000+30+8)

4.6.3. Interest on other types of accounts in Banks:

What do people do when they receive large amount of money (on retiring from service, on sale of property, .). In some cases they may need that money at a later stage for buying of property. In such cases people normally invest such an amount in Banks for a longer period.

1. As Cumulative term deposit so that they get the invested amount along with interest at the end of maturity (CTD)

2. As Fixed deposits for a fixed time so that they can earn interest regularly (FD)

4.6.3.1. Cumulative term deposit (CTD)

In this scheme a fixed amount is invested for a fixed period. The interest is paid at the end of the maturity period along with initial deposit. This scheme is suitable for those who need money after some time (buying property). The period is normally for few years. The depositor needs to make an application to bank. On payment of initial deposit bank issues a certificate to the deposit holder.

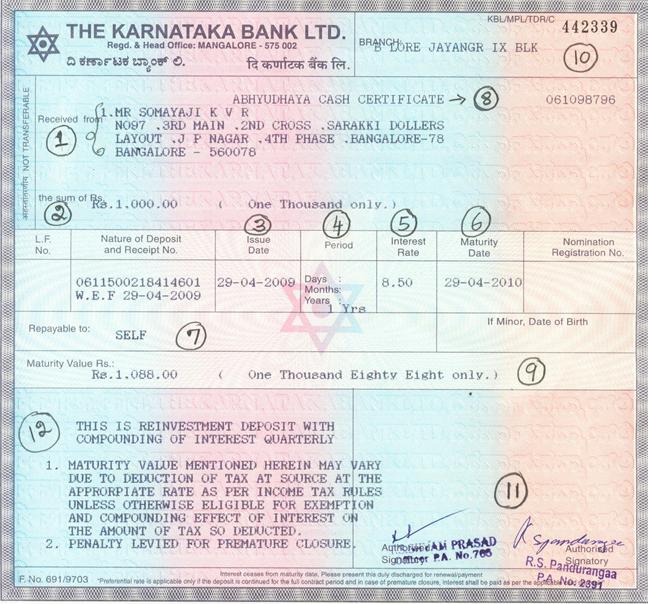

Let us look at an example of a CTD issued by Karnataka Bank

Let us understand some important details the above CTD has

|

Circled Number |

Details |

Entry in the above CTD |

|

1 |

Name and address of the person |

Somayaji, No 97, . . .Bangalore |

|

2 |

Amount of deposit in Figures and words |

Rs 1,000 One thousand |

|

3 |

Date of deposit |

29-04-2009 |

|

4 |

Period of deposit |

one year |

|

5 |

Interest Rate |

8.5% |

|

6 |

Maturity (Due) Date (The date on which Amount is payable) |

29-04-2010 |

|

7 |

Payable to whom |

Self |

|

8 |

Type of deposit |

Abhyudaya (CTD) |

|

9 |

Maturity value |

1,088 |

|

10 |

Name of branch |

Jayanagara |

|

11 |

Signature of Manager |

|

|

12 |

Other terms |

|

In the above example the depositor gets 1,088 after 1year on an investment 1,000( Thus he gets in all 88 as Interest @8.5%%)

In effect in this scheme the depositor gets interest on interest (called compound interest).

Bank uses either a formula (studied later) or a Ready Reckoner to find the compound interest

The Ready Reckoner for calculating interest for few quarters @ 9% for different amount is as given below

|

Principal |

I Quarter |

II Quarter |

III Quarter |

IV Quarter |

|

100 |

102.2500 |

104.5506 |

106.9030 |

109.3083 |

|

200 |

204.5000 |

209.1013 |

213.8060 |

218.6167 |

|

300 |

306.7500 |

313.6519 |

320.7090 |

327.9250 |

|

…. |

….. |

…… |

….. |

…… |

4.6.3.2. Fixed Deposit (FD)

In this scheme a fixed amount is invested for a fixed period and the interest is paid regularly (quarterly). This scheme is suitable for those who need money regular interest for meeting their monthly expenses. (Retired people). The period can vary from few days to few years (say 7 days to 3 years)

The depositor needs to make an application to bank. On payment of initial deposit bank issues a certificate to the deposit holder which is similar to format of CTD.

The interest is calculated using the formula:

Simple Interest = P*N*(R/100)

Where

P = Initial deposit (Principal)

N = Period (Term) of Deposit in years

R = Rate of Interest

4.6.3.3. Recurring Deposit (RD)

In this scheme, a depositor opens an account with the bank agreeing to pay a fixed amount every month for few months (three to six years)

After the maturity period, the bank pays back sum of his all monthly installment amounts and also the compounded interest. This scheme is useful for those who are in a position to save a fixed amount every month(salaried employees, fixed wage earner, shop owners…). RD accounts is helpful for those who need fairly large amount after few years for buying items( vehicles, farm equipments, ) and who have regular monthly income and can save a fixed amount every month. Normally

Banks use a Ready Reckoner to find the amount payable at the end of maturity period.

The Ready Reckoner for repayment amount for few months (6,12,24,36) for different Interest rates(6,8,10) for a monthly installment amount Rs 100 is given below.

|

Interest Rate |

6 months |

….. |

12 months |

…. |

24 Months |

36 months |

…… |

|

6% |

610.5350 |

|

1239.5234 |

|

25555.1084 |

3951.4233 |

|

|

…… |

|

|

|

|

|

|

|

|

8% |

614.0622 |

|

1252.9326 |

|

2609.1471 |

4077.1572 |

|

|

…. |

|

|

|

|

|

|

|

|

…. |

|

|

|

|

|

|

|

|

10% |

617.5972 |

|

1266.4603 |

|

2664.3955 |

4207.4544 |

|

|

…. |

….. |

|

…… |

|

….. |

…… |

|

Note : Banks prepare above Ready Reckoner after applying mathematical formula similar to

Maturity amount= P*(1+(R/100)) N + P*(1+(R/100)) N-1+ P*(1+(R/100)) N-2 + . . . P*(1+(R/100)) 1

Where P is installment amount per month. N = Number of months for which RD is opened, R= Rate of interest per month.

4.6.3 Problem 1 : If Nanda saves every month 50 Rupees for three years, find out how much she gets at the end of three years @ 8% interest and also the interest part in that amount.

Solution :

We find that for a monthly installment of Rs 50 @ 8% for 36months, the amount mentioned in the above ready Reckoner is 4077.15(rounded)

Hence at the end of 36 months she will receive Rs. 4077.15.

Since her monthly installment is Rs 50 and not 100

She will receive 4077.15*50/100 = 2038.58(rounded)

What was the sum of all her monthly installments?

Sum of monthly installment = Monthly installment*Number of months = 50*36 = 1800

![]() Total interest received = Amount

received on maturity – Sum of monthly installments = 2038.58-1800 = 238.58.

Total interest received = Amount

received on maturity – Sum of monthly installments = 2038.58-1800 = 238.58.

Note:

1. In

the above case rate of interest per month is 8/12 (![]() Rate for 12 month is

8%)

Rate for 12 month is

8%)

2. The interest % increases with the increase in period of deposit. The interest % offered by various banks is almost same.

You can visit the internet sites of the banks to know the applicable interest % for various periods at any time.

|

No. |

Features |

Recurring Deposit(RD) |

Fixed Deposit(FD) |

Cumulative Term Deposit(CTD) |

|

1 |

Opened by |

Individuals/ Business man or Companies |

||

|

2 |

Period of deposit |

Fixed number of months |

Fixed number of days |

|

|

3 |

Amount of deposit |

Fixed amount every month |

Fixed amount in the beginning itself |

|

|

4 |

Refund of deposit |

At the end of maturity period |

||

|

5 |

Payment of interest |

At the end of maturity period along with deposited amount |

Every month/3 months/6 months/year |

At the end of maturity period along with initial deposit |

|

6 |

Useful for/when |

For people with fixed income |

When in receipt/need of lump sum amount |

|

|

7 |

Minimum deposit

|

Minimum amount varies from bank to bank |

||

|

8 |

Payment of amount |

Credited to account or paid by cheque |

||

4.6.3.4. Bank loans

When banks collect deposits from public they need to find a way for disbursement (payments) of large amount of money with them. This they do so by giving loans to individuals, companies, businessmen. Like the way banks give interest to depositors on deposits, they collect interest from borrowers of loans.

The loans can be categorized as

1. Demand loans

These are loans repayable on demand. The borrower executes an agreement with the bank, promising the Bank to repay the loan at the end of loan period.

Normally loan period is of short duration less than 3 years. This type of loan is availed by individuals and ????

2. Term loans

These are similar to demand loans with the difference that term of loan is more than 36 months. This type of loan is availed by individuals and ???

In the case of above two types of loans, interest is calculated on the loan outstanding on a monthly balance basis. Interest is collected (debited) quarterly. Banks calculate daily products and on the sum of these daily products, they find the interest.

4.6.3.5. Overdrafts

This is strictly is not a loan but a financial arrangement of borrowing of amount for few days at a time. In this type of arrangement the current account holder is allowed by the bank to draw more than the balance amount in his account. The borrower and the bank agree on a upper limit. The borrower can not draw more than this limit. Overdraft facility is used mostly by traders and small businessmen when they need extra money for a short period.

In the case of overdrafts, interest is calculated on the loan amount outstanding at the close of day on a day to day basis. Interest is collected (debited) quarterly

Calculation of interest on loans

Daily product = balance * number of days the same balance was outstanding

Interest = (Sum of daily products* interest rate)/(100*365)

4.6.3 Problem 2: A person has taken a loan 1,00,000 on 15/1/01 at 12% He repays 25,000 on 18/2/01 and Rs 10,000 on 16/03/01 and 40,000 on 28/4/01. The loan was closed on 16/5/01. Calculate the interest compounded quarterly.

Solution :

We first need to find the balance amount for each of the days from 15/1/01(Loan taken date) to 28/4/01(Loan repayment date) as follows

|

Loan amount balance |

Remarks |

From date |

To Date |

Number of days |

Daily product = Balance*Number of days |

|

100000 |

Initial loan |

15/01/01 |

17/02/01 |

34(=17+17) |

3400000=100000*34 |

|

75000 |

Balance reduced on 18/02/01 because of repayment of 25000 |

18/02/01 |

15/03/01 |

26(=11+15) |

1950000= 75000*26 |

|

65000 |

Balance reduced on 16/03/01 because of next repayment of 10000 |

16/03/01 |

31/03/01 |

16 |

1040000=65000*16 |

|

Since the interest is compounded quarterly, we need to calculate the interest up to the calendar quarter ending 31/03/01. |

|||||

|

|

Sum of daily products =6390000(=3400000+1950000+1040000) Interest = (Sum of daily products* Interest rate)/(100*365) = (6390000*12)/(100*365)= 2100.82 ( rounded to 2100) Thus the amount outstanding as on 01/04/01 is 67100 ( = 65000 loan + interest of Rs 2100) |

||||

|

67100 |

Balance increased by interest of Rs 2100. |

01/04/01 |

27/04/01 |

27 |

1811700 =67100*27 |

|

25000 |

Balance reduced on 28/04/01 because of repayment of 40000 |

28/04/01 |

15/05/01 |

18(=3+15) |

450000=25000*18 |

|

0 |

Loan closed on 16/05/01 |

|

|

|

|

|

|

Sum of daily products =2261700(=1811700+450000) Interest = Sum of daily products* Interest rate/100*365 = (2261700*12)/(100*365) = 743.57 |

||||

Thus the total interest paid = 2100.82+743.57 = 2844.39

4.6 Summary of learning

|

No |

Points learnt |

|

1 |

Method of calculation of interest on SB account in Banks and Post offices |

|

2 |

Method of calculation of interest on loans |