4.4 Banking:

General introduction

to Banking.

Have you been to any Bank? You must have observed

many activities there. Some may be depositing (putting in) money and others may

be withdrawing (taking out money). Also, you must have heard people speaking about

words interest, loan, Cheque, Demand Draft (DD).

Have you heard people saying that interest they get

is too low and it is difficult to meet household expenses? For them interest is

an income used for daily living.

You need money to start a business or to buy items.

We can borrow money from people or organizations. Bank is one such institution

which lends money to borrowers. The borrowers could be individuals, companies

etc. Individuals need money to construct houses, to purchase houses, sites, items such as TV, Fridge,

Motor Cycles, cars, etc,. . Farmers also need money for buying land, cattle,

fertilizers, tractors and farm equipments. People need money to start business.

Companies also require money to expand their business. Students also need loans

for higher studies. Many others need money for marriages and for other social

functions. Banks give money to all these types of borrowers. But can Banks give

money free? Banks also have expenses

(pay salary to their employees, pay rent for building, pay for electricity, pay

for buying computers …,). Interest on loan is the extra charge that banks

collect from borrowers to meet these expenses and make some profit. How do

banks get money to give it to borrowers?

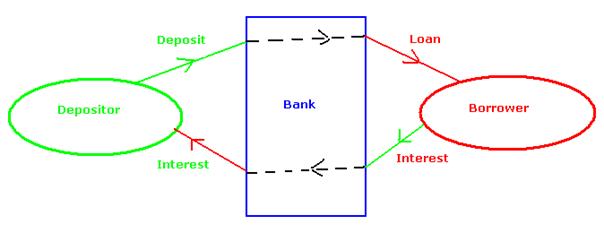

They collect money from depositors who have some

extra money (from their savings). Will these depositors give money to Bank

free? The depositors also need some incentive (encouragement), so that they can

give money to Banks. Thus, Bank is an organization that collects money from

depositors and gives money to borrowers. To encourage depositors to give money,

banks give ‘interest’ to depositors on the money they give to the Bank.

Similarly, bank charges ‘interest’ from people who borrow money from the Bank. So we can say that the Bank acts as ‘middleman’

between those who have extra money (depositors) and those who need money

(borrowers).

Karnataka Bank, State Bank of Mysore (SBM),

Syndicate Bank, Canara Bank, Citi Bank, HSBC Bank are some of the examples of Banks operating in

Banks need a system with which they can record the

transactions of their customers (depositing money and withdrawing money). For

this reason, every individual or company needs to open an account in the

Bank. At the time of opening account,

Banks check the background of individuals by asking them to produce a few

documents (Address proof, Date of birth proof….).

When an account is opened, Bank gives a unique

number to each depositor called ‘Account Number’.

When an individual opens an account he is given a ‘Savings

Bank Account’. When a company opens an account it is given a ‘Current Account’. When a businessman opens an account

he is given a ‘Current Account’.

Depending on the needs of the account holder,

accounts are mainly classified as:

1. Savings Bank (SB) account

2. Current Account (CA)

3. Recurring Deposit Account (RD)

4. Fixed or Term Deposit (FD)

5. Cumulative Term Deposit (CTD)

Opening

of an account

As an example let us look at how to fill an

application to open an SB account in Karnataka Bank. The procedure and the

application form used for opening accounts are more or less the same in all

banks. The person opening an account

needs to know a person called the introducer, who also should be known to the

Bank. This introducer needs to certify that the account opener is known to him

for a few years. This way the bank ensures that the person opening an account

is a responsible person and is unlikely to cheat the bank.

The requirements for opening an account are:

1. Completed application form.

2. Photos of the individuals opening the account.

3. Initial deposit amount.

4. Copy of Voter ID card; ration Card, Driving

License or pass port as proof of address.

5. Specimen signature card.

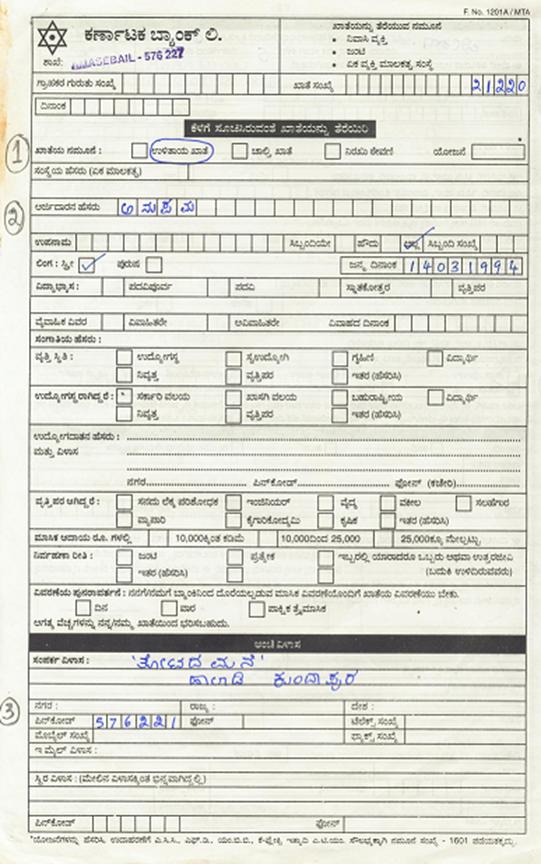

The front page of the application form looks

similar to as given below.

In the form, the photo of the individual who is

opening the account needs to be affixed in the space provided.

The photo helps in identifying the account holder

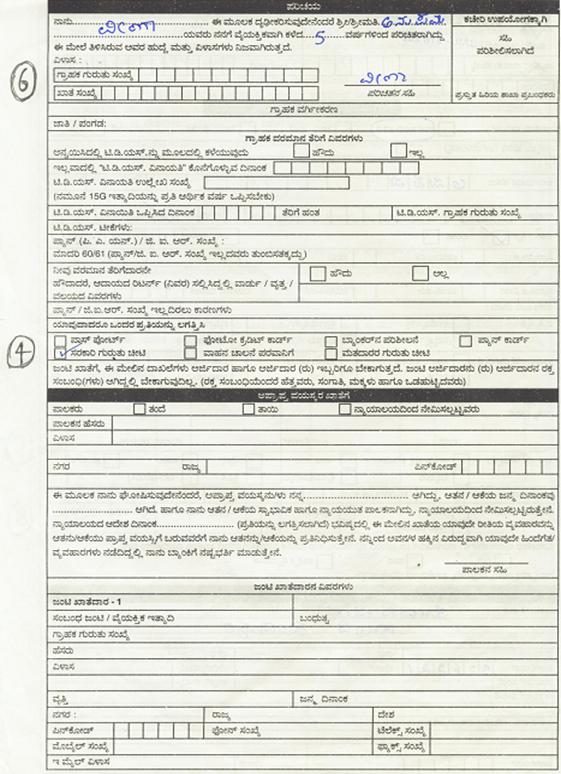

The2nd page of the Account opening form looks as

given below.

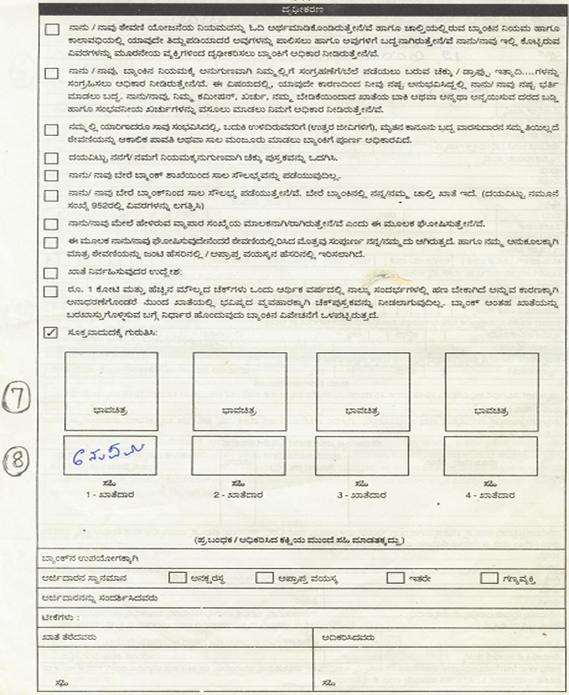

The third page is of the form

.

|

Circled Number |

Details |

Entry in the above form |

|

1 |

The

type of account |

Savings

bank |

|

2 |

Name

of the account holder |

Anupama |

|

3 |

Address

(proof such as voter ID card, Ration card. are to be submitted to the bank) |

|

|

4 |

Proof

of identity |

|

|

6 |

Name

of the introducer and How many years since the account opener is known to the

introducer. |

Veena and 5 Years |

|

7 |

Photo

of account holder |

|

|

8 |

Signature

of account holder |

Signature

of Anupama |

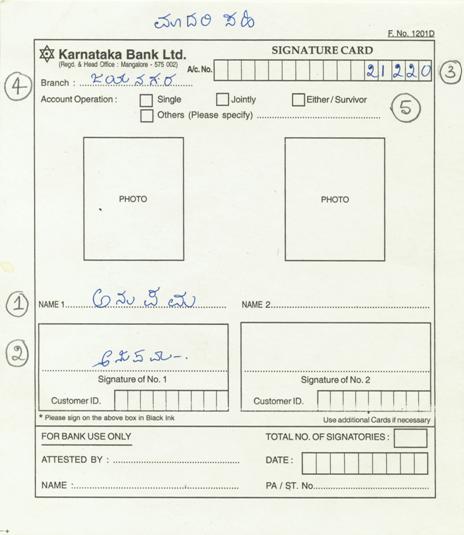

Bank maintains a Card which has two specimen

(sample) signatures of the account holder. Normally banks scan the signature

and store them in computer.

An example of the card used by Karnataka Bank is

given below

|

Circled Number |

Details |

Entry in the above card |

|

1 |

Name of the account holder |

Anupama |

|

2 |

Specimen

signature |

|

|

3 |

Account

Number given to the account holder |

21220 |

|

4 |

Branch

Name |

Jayanagara |

|

5 |

Mode

of account operation |

|

Now an SB account can be opened by Anupama after making an initial deposit.

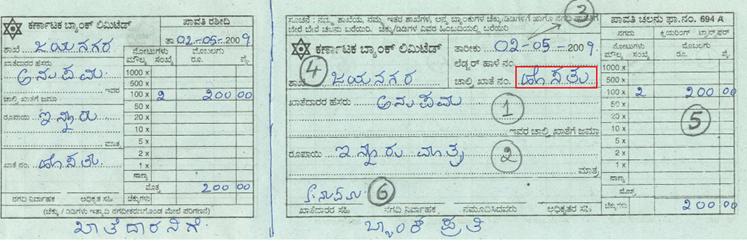

To deposit an amount into an account, we use a slip

called ‘pay in slip’. While depositing

money we need to give the bank some details

As a sample, the slip used by Karnataka Bank is

given below:

Note that the slip has two parts. Right side is for

the Bank’s use and left side is for the Depositor’s record

Let us understand the details to be filled up on

the Bank Copy. Most of the same information is filled up on the left side also.

|

Circled Number |

Details |

Entry in the above slip |

|

1 |

A/C Holders name |

Anupama |

|

2 |

Amount

of deposit in words |

Two

Hundred only |

|

3 |

Date

(of deposit) |

02-05-2009 |

|

4 |

Name

of the Bank’s Branch |

Jayanagar |

|

5 |

Amount

of deposit in figures |

200 |

|

6 |

Signature

of Depositor |

Signature |

Note: Since authorization is not

required for depositing money, any one can deposit to any one’s account.

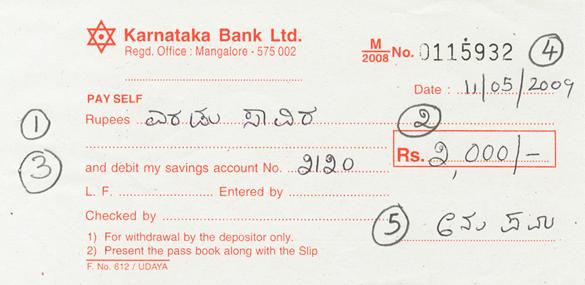

We need to

provide certain details to bank when we want to take out money from the bank

and we provide these details in the ‘Withdrawal

form’

As an example let us see what needs to be filled,

to withdraw money from the bank using the withdrawal form of Karnataka Bank.

|

Circled Number |

Details |

Entry in the above slip |

|

1 |

Amount

of withdrawal in words |

Two

Thousand |

|

2 |

Amount

of withdrawal in figures |

2000 |

|

3 |

Account

Number in the Bank |

2120 |

|

4 |

Date

(of withdrawal ) |

11-05-2009 |

|

5 |

Signature

of Depositor |

Signature(It

should be as per specimen signature card

given to the bank) |

There are some restrictions on the use of

withdrawal slip. They are:

1. Only the account holder can use this slip to

withdraw the amount for himself

2. This form can not be used to make payment to

others.

3. Account holder has to produce the pass book

Since the withdrawal slip cannot be used to make

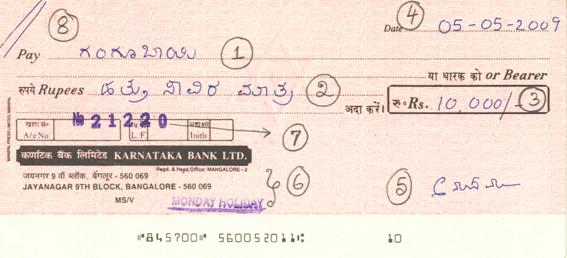

payment to others, we use a form called cheque.

Let us see what needs to be filled in a cheque so

as to pay money to others. As an example let us study the cheque format used by

Karnataka Bank. In the cheque we write certain

details which are needed to make payments

|

Circled Number |

Details |

Entry in the above cheque |

|

1 |

Pay

( Name of the person who needs to be paid) |

Gangubai |

|

2 |

Rupees(The

amount to be paid in words) |

One

Thousand only |

|

3 |

Rs. (The amount to be paid in Figures) |

1000 |

|

4 |

Date

( Date on which the money is to be

paid) |

05-05-2009 |

|

5 |

Signature

of the person issuing cheque |

Signature(It

should be as per specimen signature card

given to the bank) |

|

6 |

Branch

Name(The branch where the person who

is signing the cheque is having the account) |

Karnataka

Bank, Jayanagara |

|

7 |

Account

Number of the person issuing cheque |

11987 |

|

8 |

Mode

of Payment |

A/C

Payee |

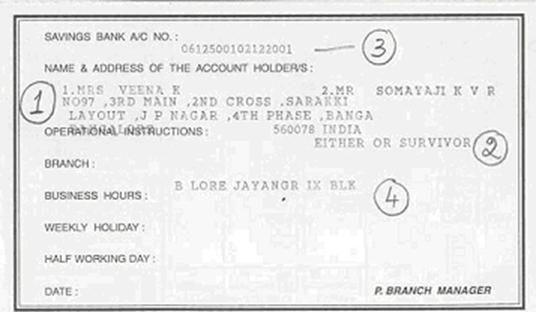

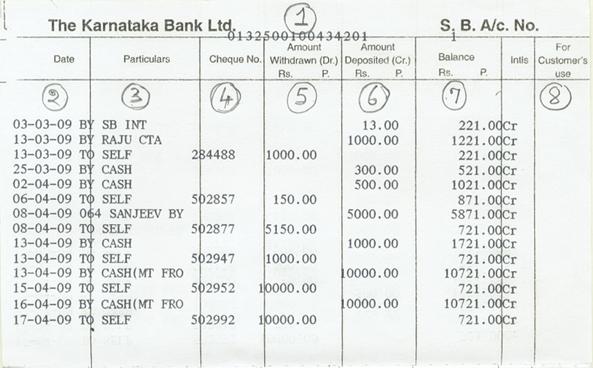

When an account is opened with a bank the bank

gives a pass book which lists the transactions carried out in that account

Almost all the banks have similar formats for pass

book.

As an example, let us look at the pass book entry

of an account holder of Karnataka Bank which is given below.

The front page of the pass book looks like this:

The front page of the passbook specifies the name of the account

holder and the account number. In the above example the account number is

21220. The inside page of the pass book looks like:

|

Circled Number |

Details |

Entry in the above pass book |

|

1 |

Name

and address of the Account holder |

Veena and Somayaji K.V.R 97. . . jayanagara |

|

2 |

Mode

of account operation |

Any

one |

|

3 |

The

Account number |

0612500102122001 |

Note that since this account is in two names, the

account is called a ‘joint account’

The next and subsequent pages give the details of

the transactions carried out by account holder.

Let us assume that this account holder does

following transactions.

TABLE 1:(The previous page

has account balance of Rs 208.00)

|

Date

of Transaction |

Details |

Reference

Number |

Amount taken out

- |

Amount

put in + |

Balance |

|

2 |

3 |

4 |

5 |

6 |

7 |

|

03/03/09 |

SB

Interest |

|

|

13.00 |

221.00 |

|

13/03/09 |

By

Raju |

|

|

1000.00 |

1221.00 |

|

13/03/09 |

To

Self |

284488 |

1000.00 |

|

221.00 |

|

25/03/09 |

By

Cash |

|

|

300.00 |

521.00 |

|

02/04/09 |

By

Cash |

|

|

500.00 |

1021.00 |

|

06/04/09 |

To

Self |

502857 |

150.00 |

|

871.00 |

|

.

. . . |

.

. . |

.

. . |

.

. . |

.

. . |

.

. . |

|

|

|

|

|

|

|

These transactions appear in the pass book as given

below

|

Circled Number |

Details |

Explanation |

|

1 |

A/c

Number |

0132500100434201 |

|

2 |

Date

of Transaction |

The

date on which money was deposited or withdrawn. |

|

3 |

Details |

How

the money has come in to the account or to whom money has been given, and how

it was taken out. |

|

4 |

Reference

Number |

The

internal number used by bank or the cheque number of the cheque. |

|

5 |

Amount taken out

- |

Amount

withdrawn from the account. This reduces the money available in the account. |

|

6 |

Amount

put in + |

Amount

deposited in to the account. This increases the money available in the

account. |

|

7 |

Balance |

The

balance amount in the account on a particular day. |

The difference between various types

of accounts can be summarized as follows:

|

No. |

Features |

Savings Bank Account(SB) |

Current Account(CA) |

|

1 |

Opened by |

Individuals |

Businessman

or Companies |

|

2 |

Maturity period |

Operative till it is closed |

|

|

3 |

Deposits Use |

No limit |

|

|

4 |

Use |

For Daily use |

|

|

5 |

Withdrawals |

Fee

may have to paid if number of withdrawals exceed the limit |

No

restriction |

|

6 |

Interest |

The

balance in the account earns monthly

interest on the minimum balance maintained between 10th and

the last day of the month |

No

interest |

|

7 |

Minimum Balance |

Normally

no, But some special accounts may have

to keep specified minimum |

Can

become nil |

|

8 |

Mode of Withdrawals |

Cheque/Withdrawal

slip can be used |

Only

Cheque |

Types of

Accounts

Account in the banks or Post offices can be opened

in more than one name. ‘Joint account’ is

an account opened by more than one person .A joint account can have a maximum

of three names.

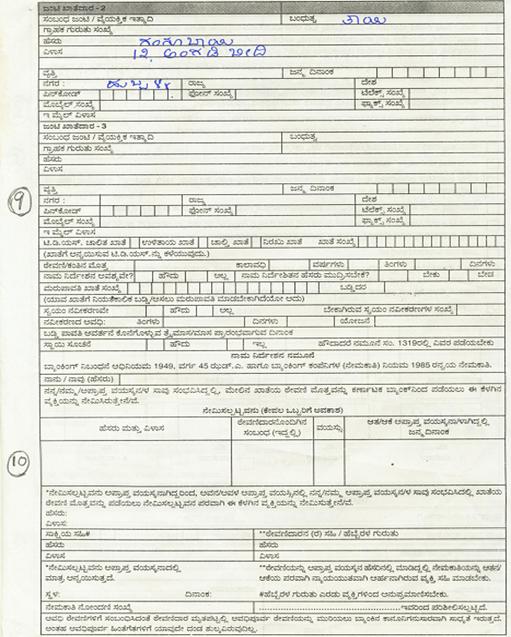

While opening the account ,names

of all the persons are to be mentioned. In such cases Specimen signature card

needs to be filled up for all the joint account holders.

In the case of operating a joint account

(withdrawal of money, signing cheques) the account holders have the following

options:

1. Any one can sign (useful when one account holder

is out of station or if he is no longer alive)

2. All need to sign (More secure as all account

holders need to sign)

The option chosen by the account holders need to be

intimated to Banks as seen in the following application.

The entries circled as number 9 indicates that

application is for a joint account (in the names of Anupama

and Gangubai)

We have seen earlier that money can be withdrawn

using either a withdrawal slip or a cheque.

Only the account holder can use a withdrawal slip

to take money out of his account. To make payments to others, only cheques can be used.

However,a cheque can also be used by an

account holder to withdraw money for himself.

There are three parties involved in the realization

(credit of amount) of cheques

1. Payee (Circled number 1):

The party who receives the amount mentioned in the cheque (In the above example

it is Gangubai)

2. Drawer (Circled number 7,

5): The party which pays the amount mentioned in the cheque (In the

above example it is the account holder of account 21220–Name not known/mentioned)

2. Drawee (Circled number 6):

The Bank which pays the amount on behalf of drawer (In the above example

it is Karnataka Bank)

Process

of crediting the amount mentioned in the cheque

Let us assume that you (Suman)

have received a cheque from your friend (Nanda) say for Rs 1000/-. In this case

you are the Payee and your friend Nanda is the drawer

Assume that your banker (where you have an account)

is Karnataka Bank and Nanda’s banker is Canara Bank.

The following sequence of operations take place

before Rs 1000 is credited to your account

1. You deposit the cheque in Karnataka Bank using the

deposit slip

2. Your banker (Karnataka Bank) sends the cheque to

the banker of Nanda (Canara Bank.)

3. Canara Bank checks if the cheque can be cleared

(passed) or not

4. If the cheque is passed by Canara Bank then

Canara Bank debits the account of Drawer (Your friend) for Rs 1000 and informs Karnataka

bank that cheque is passed.

5. Karnataka Bank credits the amount of Rs 1000 to

the account of Payee (You)

The above process is called ‘Cheque clearance’.

If Payee and

Drawer have their accounts in the same city/town the amount is normally

credited to the account of Payee in 2 or 3 days. In case of outstation cheque

it may take several days.

Passing

of cheque

You would have heard the term ‘bouncing of cheque’ or ‘dishonoring of cheque’.

It means that the receiver of the cheque can not be credited with the

amount mentioned in the cheque to his bank account.

A cheque could be dishonored due to any of the

following reasons

1. The balance in the account does not have the

amount specified in cheque

2. Signature/s on the cheque does/do not tally with

what is given to the Bank in the specimen signature card.

3. In case of joint Accounts not all people have

signed the cheque( if account is opened with joint

operation)

4. In cases of overwriting/corrections on the cheque or corrections which have not been counter signed(one more signature)

5. Cheque is post dated (Cheque

date is that of future)

6. Expired cheque date (cheque’ s validity is

normally 6 months from date of cheque)

7. The issuer of cheque has given instructions to

his banker for stopping payment – called stop payment

The Government of India has made a

law to the effect that dishonoring of cheque is a criminal offence. In such

cases the person issuing the cheque can be sent to jail.

The cheques can be drawn in two ways

1. ‘Bearer cheque’: In this case the word ‘bearer’ on the cheque is not struck. This type of cheque can be encashed by any possessor of the cheque irrespective

of the name written on the cheque. Thus in this there is a risk of amount being

paid to wrong people

In case the word ‘bearer’

on the cheque is struck and the party’s name is written then the cheque can be

encashed by any person just by signing on the reverse of cheque

. In this case also there is a risk of amount being paid to wrong

people(because any one can sign on the reverse side of the cheque)

2. ‘Crossed cheque’: In this

case the

words ‘A/C

Payee’ are written across at the top left corner of the cheque.(As in

circled number 9 in the format discussed

earlier ). This type of cheque can be encashed only by the payee (whose name is

written on the cheque) that too only after crediting the amount to the account

of payee through his banker. Thus this type of cheques is more secure and even

if the cheque is lost it is very difficult for the possessor of cheque to

encash the cheque.

The crediting of crossed cheques follows the

process of ‘Cheque clearance’ described earlier.

Thus, it is obvious that a person who

does not have a bank account, can not get the amount mentioned in a crossed

cheque, even if his name is written on the cheque (he is the payee)

Note: We use the Mode of payment as

‘A/C Payee’ when

1. The

amount is not paid immediately in cash

2. The

amount is paid only after crediting the amount to the account of the Payee.

3. Only the

person (Payee) whose name is mentioned against ‘Pay’ in the cheque can receive

the money.

4. Even if

the cheque is misused by some one there should be a way to find who received

the amount.

|

No. |

Features |

Bearer

Cheque |

Crossed

cheque |

|

1 |

Payment to receiver |

Immediate

payment |

If

the cheque is of different bank/branch/city, amount is not given immediately. |

|

2 |

Balance in the account |

Balance

> amount mentioned in the cheque |

The Account needs to have the specified

amount only at the time of cheque clearance |

|

3 |

Date of cheque |

Can

be earlier dates |

Can

be of future date |

|

4 |

Signature on the reverse side of cheque |

Must

|

No

need |

|

5 |

Security |

Not

secure(any one can get the amount) |

Secure

(we can trace the receiver of the amount) |

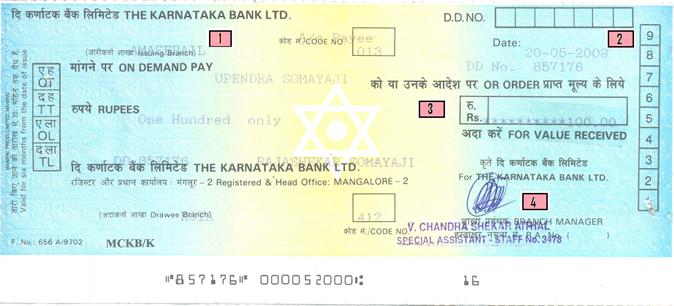

Demand

Draft:

You must have heard people talking about a getting

DD (Demand Draft), towards application fee, examination fee and for many such

payments

It is a special instrument which does not get

dishonored (bounced). It is always issued by a Bank. Given below is the copy of

a DD issued by Karnataka Bank, as can been seen from the name printed at the top. Notice that this DD is a crossed DD as ‘A/C

Payee’ is mentioned in the middle.

|

Number in the square |

Entry in the DD |

Details |

|

1 |

Amasbrail |

The

branch of bank issuing the DD |

|

2 |

20-05-2009 DD

N0.857176 |

Date

of issue of DD(Validity period is six months) Unique

DD Number |

|

against

‘ON DEMAND PAY’ |

Upendra Somayaji |

The

party which gets the amount specified in the DD |

|

3 |

100 |

The

amount payable to the party |

|

4 |

|

Signatures

of the officer/s of branch issuing DD |

Let us list the difference between

Cheques and DDs

|

No |

Features |

Cheque |

Demand Draft(DD) |

|

1 |

Issuer |

Issued

by account holder |

Issued

by bank |

|

2 |

Availability

of Amount |

The

account needs to have enough balance, at the time of passing of cheque. |

Amount

needs to be paid to the bank before DD is made |

|

3 |

Safety |

Can

be forged easily |

Highly

secure |

|

4 |

Credit

of amount to the payee’s account. |

Could

take few days |

One

or two days |

|

5 |

Dishonoring of instrument |

Cheque

may get dishonored |

Guaranteed

by Bank ,so cannot be dishonored |

|

6 |

Issue

Date |

Can

be pre/post dated |

Cannot

be pre/post dated |

|

7 |

Signature |

Signed

by Accountholder/s |

Signed

by 2 designated officers of the Bank |

|

8

|

Charges

for issue |

Nil

or negligible |

Based

on the value of DD, the Bank charges commission |

As seen from the above, DD is similar to cheque but

it is issued by the Bank. (Both Drawer and Drawee are Banks)

Because of this reason DD does not bounce and hence

it is as good as cash. For this reason, many organizations ask for payment by

Demand Draft for their products and services (issue of application forms,

payment of fees, buying of products.) and not cheques.

Banks follow the procedure of cheque clearance for

crediting DDs also, so as to avoid frauds in DDs.

Information

Technology in Banking:

1. Computerisation

:

Most of the banks have computerized their

operations which has reduced their paper work. Interest calculation, issue of

Deposit receipts, clearance of cheques and many such routine activities are performed

by computers. This has helped in increasing the efficiency of banks.

2. Electronic

fund transfer:

This is a facility where money is transferred

electronically from one account to another account without the need for issue

of cheque, DD.

In this method the amount is credited to payee’s

account immediately eliminating the need for ‘cheque clearance’ thereby saving

time.

This method is used mainly by banks for inter bank

transfer and by many companies.

3. ATM:

You must have seen people withdrawing money not

from banks but from machines called ATMs (Automatic Teller Machines) from

anywhere, any time.

When a person opens an account with the bank, most

of the banks issue an electronic card called ATM card. Along with card the

depositor is also provided a password( Secret code).

Once the card is inserted into an ATM machine, it asks for the password. If

correct password is entered then the person can do the following activities:

·

Withdraw cash up to a limit (Could be Rs 10,000 per day)

·

Check the balance

·

Change original password

·

Take print out of passbook (limited transactions)

·

Request for issue of cheque book

…….

This card contains depositor’s name, account

number, validity period for usage of card

This facility has been made possible because of

computerization in Banks and interlinking of branches of Banks (Connectivity).

4. Internet

Banking:

Quite a few banks have introduced this facility

which allows depositors carry out following activities from any where in the world

any time through the internet

·

Check the balance in account

·

Print/view the account transactions(pass book)

·

Request for issue of cheque book

·

Request for issue of DD

·

Stop payment

·

……….

Exchange

Rates:

We are familiar that each country has its own

currency. Since companies carry out business with other countries (export,

import)

Money received/to be paid needs to be converted to

local currencies.

The rate at which one currency is converted to

another currency is called ‘exchange rate’

This exchange rate changes on daily basis depending

upon the economy, market conditions, global crisis and other external factors

These rates are published in many newspapers

Some of the popular currencies and exchange rate as

on October 12, 2006 is given below.

|

No |

Country |

Currency |

Rate in Rs. |

|

1 |

|

Dollar |

45.7 |

|

2 |

|

Pound |

85.26 |

|

3 |

Part

of |

Euro |

57.55 |

|

4 |

|

|

28.95 |

|

5 |

|

Yen

|

00.383 |

|

6 |

|

Riyal |

12.31 |

4.4 Problem 1 : If an Indian company

wants to import goods worth 1000 Dollars from the

Solution:

Since 1Dollar = Rs. 45.7

1000 Dollar = 45.7*1000 = Rs45,700

Since the supplier accepts only Dollars, the

company pays Rs 45,700 to the bank to get the equivalent amount in dollars.

4.4 Problem 2 : If an Indian company

exports goods worth Rs1,00,000 to a Japanese company. Find out

how many yen it has to mention in the bill given to the Japanese company.

Solution:

Since Rs. 00.383Rs = 1 yen

1,00,000 rupees = 100000/00.383 = 2,61,097 yens

This is the amount in yen which company has to

mention in the bill.

4.4 Summary of learning

|

No |

Points learnt |

|

1 |

Various

forms(instruments) used by banks in respect of

operation of an account in a Bank. |