4.7 Compound Interest

We have seen earlier the formula for SI as

Simple Interest (SI) = P*N*(R/100)

Where

P = Principal

N = Period

R = Rate of Interest

4.7 Example 1 : If a person deposits

Rs 10000 in a Bank as an FD for one year, how much interest does he

get after one year and after 2 years?

Workings:

In this Problem P =10000 R=6 and N=1

![]() Simple Interest for one year = P*N*(R/100) = 10000*1*6/100 =

600

Simple Interest for one year = P*N*(R/100) = 10000*1*6/100 =

600

If the period is 2 years then N=2

![]() Simple Interest for 2 years = P*N*(R/100) = 10000*2*6/100 =

1200

Simple Interest for 2 years = P*N*(R/100) = 10000*2*6/100 =

1200

Assume in the above case, the depositor chooses not

to receive the interest after one year

but requests the bank to pay him interest at the time of maturity of deposit

(I.e. after 2 years). In such a case should bank pay him more interest than Rs

1200?

Bank does pay him little more. It pays interest on

the first year interest (Rs 600) at the same rate of 6%. Why does bank pay

extra? This is because, Bank has used the interest amount for one year for it’s

activities and hence bank

is bound to give interest on interest. This is called ‘compound interest’.

In case of

simple interest, the principal amount remains constant throughout, whereas in

the case of compound interest, the principal amount goes on increasing at the

end of the period (term).

Let us calculate

simple and compound interest for an initial deposit of Rs 10,000.

N =1, R =6

|

|

I year |

II year |

|

Principal in the beginning of the year

(P) |

P=10000 |

P=10600 (Amount at the end of I year becomes

new principal) |

|

Interest for one year (SI) |

PNR/100 = 10000*1*6/100 = 600 |

PNR/100 = 10600*1*6/100 = 636 |

|

Amount at the end of year (P+SI) |

10600(=10000+600) |

11236(=10600+636) |

Total interest will be 1236 (=600+636)

Thus, the depositor gets Rs 36 extra interest in

the compound interest when compared with simple interest

The formula used for calculating compound interest

is given below

Maturity Amount = P*(1+(R/100)) N

Compound Interest (CI) =

Maturity Amount – Initial deposit =P*(1+(R/100)) N-P

4.7 Exercise : Use the above formula to verify that CI on Rs 10000 for two years @ 6% is indeed

1236

Let us find

the difference between Simple interest and Compound interest for 5 years on a

deposit of Rs 10000 at 9%

We will be

using the above formulae for SI and CI with P =10000, R= 9 and N = 1 to 9

Compound

interest for 5 years = P*(1+(R/100)) N-P = 10000*(1+(9/100)) 5-P

= 15386.24 -10000 =5386.24

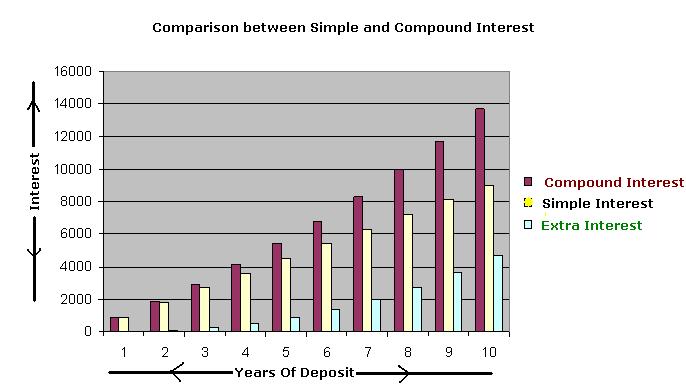

Table:

Comparison of SI and CI On a Principal of Rs 10000 @R=9% for 1 year to 9

years ( Calculator was used for working)

|

Number

of Years --à |

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

|

Compound

Interest(CI) |

900 |

1881 |

2950.29 |

4115.82 |

5386.24 |

6771 |

8280.39 |

9925.63 |

11718.93 |

|

Simple Interest(SI) |

900 |

1800 |

2700.00 |

3600.00 |

4500.00 |

5400 |

6300.00 |

7200 |

8100 |

|

Extra interest |

0 |

81 |

250.29 |

515.82 |

886.24 |

1371 |

1980.39 |

2725.63 |

3618.93 |

The above table can be represented in a bar chart

as given below.

(Colors of numbers in the table match with Colors of

bars in the chart: CI, SI and Extra interest)

|

|

We clearly

see the benefit of compound interest on deposits. The benefit increases with

the increase in the term of the deposit.

Note that Compound

interest is paid to the depositor in the case Fixed and Cumulative Term

Deposits (FD,CTD)

Do you

observe that the initial deposit nearly doubles?

With compound

interest @ 9%, interest paid in 8 th year is equal to initial deposit and hence the original amount doubles in 8 years

Exercise Using the formula for CI, check that the principal amount doubles

(Interest =Principal) with the rate and approximate period (number of years) as

mentioned below:

Table : Rate of interest and period combination for

the principal amount to double

|

Rate% ----> |

7 |

8 |

9 |

10 |

11 |

12 |

|

Approximate

years required for doubling of

Principal |

10 Years 3 Months |

9 years |

8 Years |

7 Years 3 Months |

6 Years 9 Months |

6 Years 2 Months |

Normally

compound interest is calculated quarterly and hence the initial deposit doubles

in a lesser period than mentioned above.

The Banks

also use pre calculated table of interest called Ready Reckoner for calculating

compound interests for different periods and different rates.

Note that

Banks always charge compound interest on any type of loan taken by borrowers

4.7 Problem 1: Let us take the case of

Ram (4.5 Example 1) wherein he decides not to take interest from the bank

yearly. He chooses the option of

investing Rs. 5000 in the bank

for 6 years as a cumulative deposit at the rate of 8% compounded

interest. Let us calculate how much does he get at the end of 6 years

Solution :

P= 5000

R =8

N=6Years

Maturity Amount = 5000(1+8/100)6 =

5000*1.08*1.08…(in all 6 times) =7934.37

Compound interest = maturity amount -deposit amount

=7934.37-5000=2934.37

Thus in all he gets Rs. 2934.37 as cumulative

interest. Compare this with Rs. 2400 he gets as total interest in simple

interest method (4.5 Example 1). In compound interest method he gets Rs 534.37

extra.

Thus cumulative fixed deposit is useful for people

who do not need interest money often and who are willing to wait for the total

amount to be received at the end of maturity period.

In the above Problem we had calculated compound

interest yearly (interest on interest was calculated once a year). However

Banks calculate the compound interest quarterly (i.e. once in three months).

Since a year has 4 quarters, Banks calculate Compound interest four times in a

year.

4.7 Problem 2: Simple interest on a

sum of money for 2 years at 6.5% per annum is Rs5200. What will be the compound

interest on that sum at the same rate for the same period?

Solution:

We need to find

the principal in order to calculate CI

Let P be the

principal

We know

SI = (P*n*R) /100

= P*2*(13/2)/100 = 13P/100

It is given

that SI= 5200

![]() 5200 = 13P/100

5200 = 13P/100

![]() P = 5200*100/13 =

40000

P = 5200*100/13 =

40000

![]() Maturity Amount= P*(1+(R/100)) N = 40000*(1+13/200)2

= 40000*(213/200)*(213/200) = 213*213 = 45369

Maturity Amount= P*(1+(R/100)) N = 40000*(1+13/200)2

= 40000*(213/200)*(213/200) = 213*213 = 45369

![]() CI = Maturity amount –

principal = 45369-40000 = 5369

CI = Maturity amount –

principal = 45369-40000 = 5369

Verification:

SI = (P*n*R) /100 = 40000*2*(13/2)/100 = 40000*13/100 = 5200 which is the Si

given in the problem, hence our value for Principal is correct.

4.7 Problem 3: The difference between

Compound interest and simple interest on a certain sum for 2 years at 7.5% per

annum is Rs 360. Find the sum

Solution:

We need to

find the principal in order to calculate CI

Let P Be the principal amount

SI = (P*n*R)

/100 = P*2*(15/2)/100 = 15P/100

Maturity Amount= P*(1+(R/100)) N =

P*(1+15/200)2 = P*(215/200)*(215/200) = P*46225/40000

![]() CI = Maturity amount –

Principal = 46225P/40000 –P

CI = Maturity amount –

Principal = 46225P/40000 –P

It is given that CI-SI = 360

![]() 360 = 13325P/40000 –P

– 15P/100 = (46225P -40000P -6000P)/40000 = 225P/40000

360 = 13325P/40000 –P

– 15P/100 = (46225P -40000P -6000P)/40000 = 225P/40000

![]() P = 360*40000/225

= 64000

P = 360*40000/225

= 64000

Verification:

SI = (P*n*R) /100 = 64000*2*(15/2)/100 = 64000*15/100 = 9600

Maturity Amount= P*(1+(R/100)) N = 64000*(1+15/200)2

= 64000*(215/200)*(215/200) = 64000*46225/40000 = 73960

CI = Maturity amount – Principal =73960 -64000 =

9960

![]() CI-SI = 9960-9600 =360

which is as given in the problem and hence our value for P is correct.

CI-SI = 9960-9600 =360

which is as given in the problem and hence our value for P is correct.

4.7 Problem 4: Rekha invested a sum of

Rs 12000 at 5% Interest compounded yearly. If she receives an amount of Rs

13230 at the end of n years find the period

Solution:

Let n be the period

![]() Maturity Amount== P*(1+(R/100)) n = 12000*(1+(5/100))

n = 12000*(1+1/20)n =

12000*(21/20)n

Maturity Amount== P*(1+(R/100)) n = 12000*(1+(5/100))

n = 12000*(1+1/20)n =

12000*(21/20)n

It is given that maturity amount is 13230

![]() 13230 = 12000*(21/10)n

13230 = 12000*(21/10)n

![]() (21/10)n=13230/12000

= 411/400 = 21*21/(20*20) = (21/20)2

(21/10)n=13230/12000

= 411/400 = 21*21/(20*20) = (21/20)2

![]() n =2

n =2

Verification: By substituting value

of n and others in the formula for CI, find out that amount received is 13230.

4.7 Problem 5: At what rate per cent

compound interest, does a sum of money become 2.25 times itself in 2 years?

Solution:

Here N=2. Since we are given that amount becomes

2.25 times in 2 years, A =2.25P.

Let P be the Principal and R be the rate to be

found

A = P*(1+(R/100)) N= P*(1+(R/100))2

Since A =2.25

2.25P = P*(1+(R/100))2

![]() 2.25 =9/4 =(1+(R/100))2

2.25 =9/4 =(1+(R/100))2

Since 9/4 =(3/2)2

We have 3/2 = (1+(R/100)

On simplification we get R/100 = 1/2

![]() R = 50

R = 50

Verification: We have N=2, R=50

and Let P be the principal amount

![]() A = P*(1+(R/100)) N= P*(1+(50/100))2

=P*(150/100)2 = P*(3/2)2 = P*9/4 = 2.25P which is as

given in the problem.

A = P*(1+(R/100)) N= P*(1+(50/100))2

=P*(150/100)2 = P*(3/2)2 = P*9/4 = 2.25P which is as

given in the problem.

Application

of Compound interest formula other than in Banking:

Normally, companies buy machinery and equipments

for their use. Because of the usage, the value of the machine reduces over a

period.

This is the reason why second hand machine or vehicle

is available at a lower price.

This is reduction in value is called ‘depreciation’. The rate at which the value reduces

is called ‘rate of depreciation’.

If the cost of machine or equipment depreciates at

the rate of R% every year its value after N years is given by the formula

Value after N years = (Present value)*(1-(R/100))

N

Conversely

The present value of machine = (It’s value N years

ago) *(1-(R/100)) N

4.7 Problem 6 : The current population of a town is 16,000. It is estimated that the

population of the town to grow as follows:

First 6 years

@ 5%

Next 4 years

@8%

Find out the

population after 10 years

Solution:

We use the formula for CI for finding out population

after 10 years :

Population after N years = (Present population)*(1+(R/100))

N

Conversely

Present population = (Population N years ago) *(1+(R/100))

N

Step1: First

find out population at the end of 6 years. (Here P=16000, N=6, R=5)

Population at the end of 6 years

= P*(1+(R/100)) N

=

16000(1+5/100)6

= 21445

Thus at the

end of first 6 years population is likely to be 21,500

Step 2: Find

out population at the end of 4 years. (Here P=21500, N=4, R=8)

Population at

the end of 4 years

= P*(1+(R/100)) N

=

21500(1+8/100)4

= 29250

Thus 29,250

is the likely population of the town after 10 years.

4.7 Problem 7: Have you not observed a rubber ball losing height on each bounce? Let us

say that each time a rubber ball bounces , it raises only to 90% of its

previous height. If it is dropped from the top of 25 meter tall building, to

what height would ir rise after bouncing the ground 2 times

Hint : (As in depreciation)

Since ball raises only

90% of its previous height on the next bounce, we could say it loses(depreciates)

10% of its previous value

Thus P=25, R =10

Hence the formula

Height raised after two

bounce = 25((1-(10/100))

2 = 20.25m

While calculating the compound interest,

when the interest is compounded at different periodicity other than every year,

the formula for compound interest calculation changes slightly.

|

When

interest is compounded |

Yearly |

The

Principal changes |

Every year |

Interest is calculated once

a year(t=1) |

|

Half yearly |

The

Principal changes |

Every half year |

Interest is calculated twice a year(t=2) |

|

|

Quarterly |

The

Principal changes |

Every quarter |

Interest is calculated four times a year(t=4) |

|

|

Monthly |

The

Principal changes |

Every month |

Interest is calculated twelve times a year(t=12) |

Let R be the rate of interest per annum and N be

the number of years for which the interest is calculated and t be the periodicity(year, half

yearly, quarterly, monthly) with which compound interest is calculated.

Then the formula for maturity amount changes to

A = P*(1+(R/t*100)) N*t

Note:

The above change in formula is due to the fact

that, the rate per year is converted to rate per half year(R/2), rate per

quarter(R/4), rate per month(R/12) if the interest is calculated half yearly(2

times), quarterly(4 times) or monthly(12 times) respectively. Also, note that

in such cases N changes to 2N, 4N and 12N respectively.

4.7 Problem 8: What is

the maturity amount on Rs 50,000 placed with the bank if it pays 6% compounded

interest for the first three years and 7% for the next two years with interest compounded

every quarter.

Hint: As in 4.7 Problem 6, solve the problem in two steps as shown below by

using the formula A = P*(1+(R/t*100)) N*t.

1. Calculate the maturity

amount after 3 years (12 quarters) @ 6% for three years on principal of Rs

50,000 (N=3, t=4, R=6)

2. With the maturity

amount as obtained in step 1 as principal, calculate the maturity amount for

next two years (8 quarters) @7% (N=2, t=4, R=7).

4.7 Summary of learning

|

No |

Points to remember |

|

1 |

Maturity

Value= P*(1+(R/100)) N |

|

2 |

Compound

interest = P*(1+(R/100)) N-P |